Introduction!

AR

MA:

small conclusion of AR and MA:

ARMA:

help us get deeper understanding:

We should know:

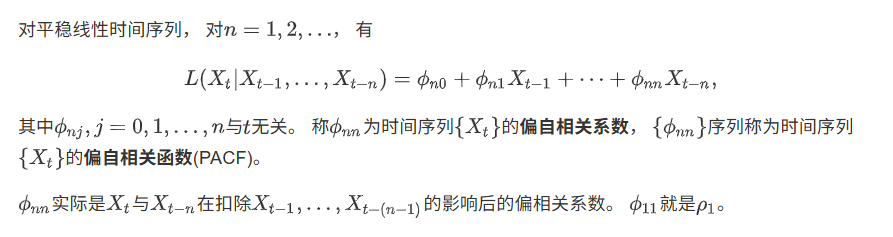

1. Autocorrelation Function (ACF) as the Primary Tool

When selecting time series models, we primarily examine the Autocorrelation Function (ACF), which measures correlation through the correlation coefficient \(\rho_k\). This is the key index for identifying dependency structures in time series data.

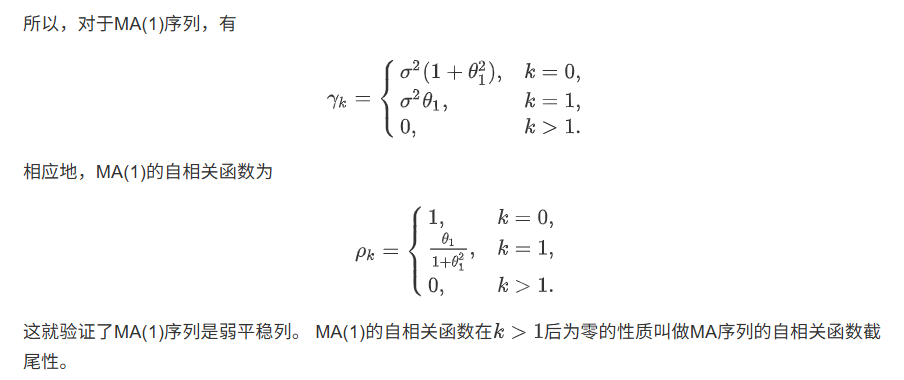

2. MA(1) Model Properties

The MA(1) model is favorable because it naturally satisfies \(\rho_k = 0\) for \(k > 1\). Consequently, we can say that MA(1) processes are \(\rho^*\)-mixing and absolutely ANA.

3. Covariance Structure Considerations

Beyond correlation, covariance (denoted as \(\gamma_k\)) is also a useful tool for constructing sequences with specific dependency properties. For example, NA requires \(\text{Cov}(X_i, X_j) \leq 0\) for all \(i \neq j\). This translates to the condition \(\gamma_k \leq 0\) for \(k \geq 1\).

4. NA Properties of Different Models

Incorrect Claim:

"If \(\phi_1 \leq 0\), then \(\gamma_k \leq 0\) for AR(1). For ARMA(1,1) with \(\phi_1 > 0\), \(\theta_1 < 0\), and \(|\theta_1| > |\phi_1|\), it will retain NA."

Correction:

This is incorrect. If a model contains an AR component, it cannot be NA due to the persistence of dependencies.

4'. (Correct Statement)

However, using similar reasoning, we can obtain NA properties from MA(1). We only need to ensure \(\gamma_1 < 0\), which is not difficult to achieve.

5. ARMA(1,1) as a Generalization

Since ARMA(1,1) generalizes both AR(1) and MA(1), its properties are more complex and require careful analysis.

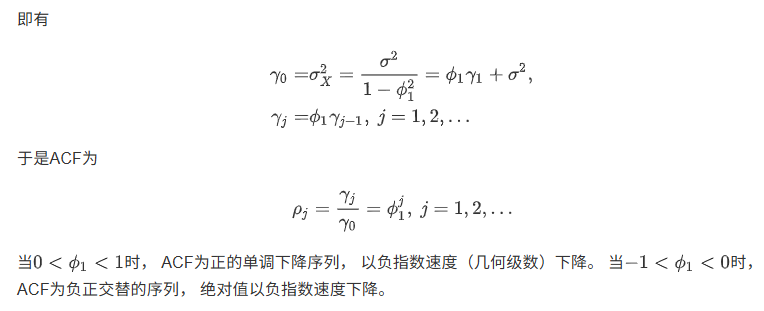

6. AR(1) Model Analysis

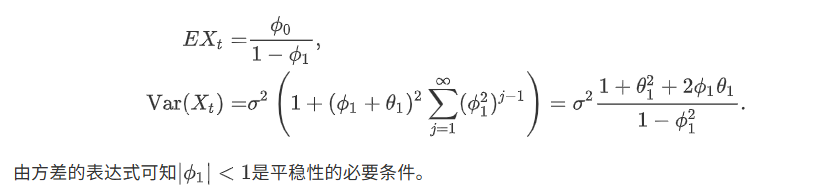

For an AR(1) process \(X_t = \phi_1 X_{t-1} + \varepsilon_t\):

-

Covariance structure:

\[\gamma_k = \phi_1 \gamma_{k-1} \quad (k = 1, 2, \ldots) \]with

\[\gamma_0 = \text{Var}(X_t) = \frac{\sigma^2}{1 - \phi_1^2} > 0 \] -

Specific covariances:

\[\gamma_1 = \phi_1 \cdot \frac{\sigma^2}{1 - \phi_1^2} \quad (\text{sign depends on } \phi_1) \]\[\gamma_2 = \phi_1^2 \cdot \frac{\sigma^2}{1 - \phi_1^2} > 0 \quad (\text{always positive}) \]

Since \(\gamma_2 > 0\) for all \(\phi_1 \neq 0\), AR(1) processes are NOT NA.

However, if \(|\phi_1| < 1\), we have \(\rho_k \to 0\) as \(k \to \infty\). Therefore, AR(1) is \(\rho^*\)-mixing and consequently must be ANA. Similarly, ARMA(1,1) processes are also not NA.

7. MA(1) Model for NA Sequences

MA(1) processes can be NA if we ensure \(\gamma_1 < 0\). This provides a practical way to construct NA sequences.

8. Summary

- AR models (containing AR components) are generally not NA but can be \(\rho^*\)-mixing and ANA under stationarity conditions.

- MA(1) models can be designed to be NA by ensuring negative first-order autocovariance.

- When selecting sequences for statistical applications, consider both correlation (\(\rho_k\)) and covariance (\(\gamma_k\)) structures to achieve desired dependency properties.

reference:

https://www.math.pku.edu.cn/teachers/lidf/course/fts/ftsnotes/html/_ftsnotes/fts-armod.html#tslin-ar-concept